BY: JANN SWANSON

Lower Rates Push Mortgage Applications to a Six-Year High

Feb 5 2020, 6:51AM

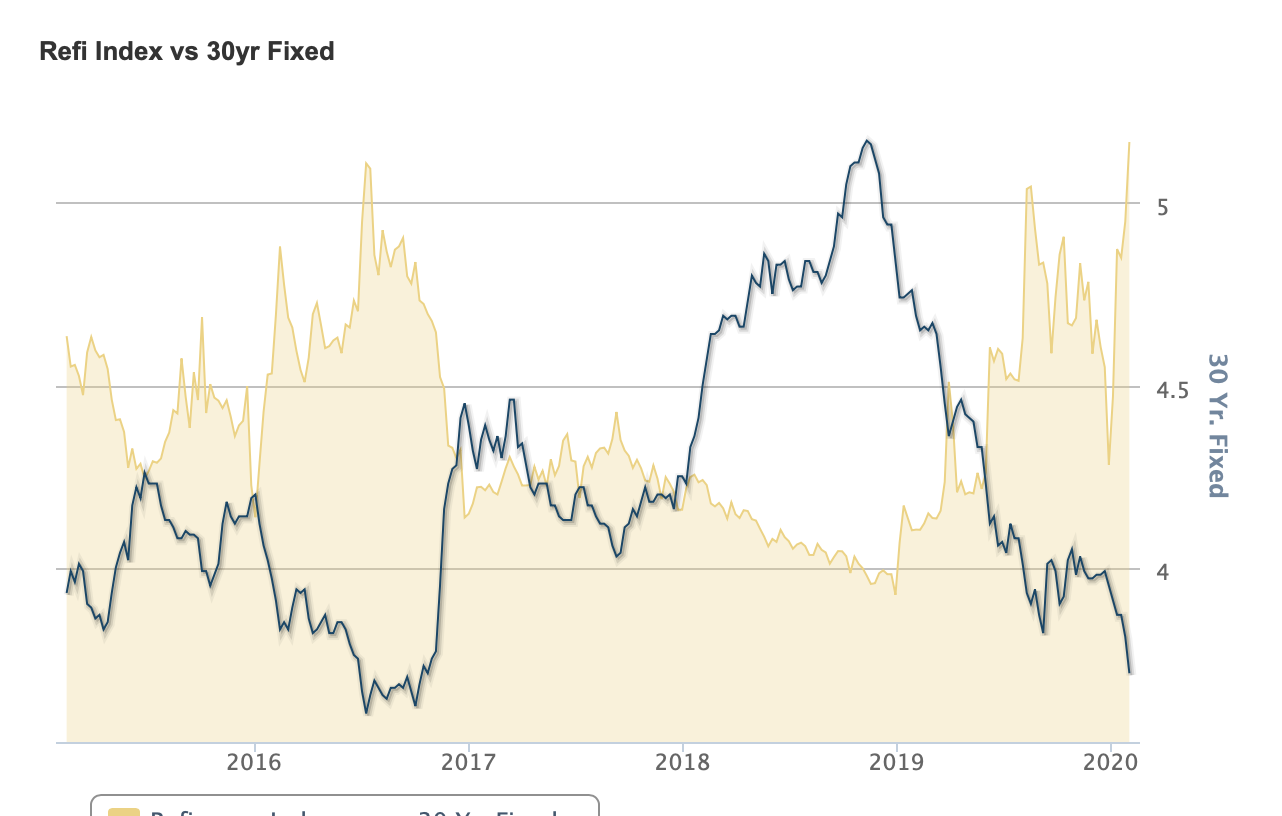

Mortgage application volume continues to benefit from lower interest rates. The Mortgage Bankers Association (MBA) said today that its Market Composite Index, a measure of that volume, reached its highest level since May 2013 last week.

The 5.0 percent gain in the seasonally adjusted index during the week ended January 31 was solely due to strength on the refinancing side. Of note, the previous week was shortened by the Martin Luther King holiday and MBA adjusted the week's results to account for the event. On an unadjusted basis the index, a measure of mortgage application volume, rose 20 percent compared with the previous week.

The Refinance Index jumped by 15 percent to its highest level since June 2013 - and was 183 percent higher than the same week in 2019. Applications for refinancing constituted 64.5 percent of the total, up from 60.4 percent the previous week.

The seasonally adjusted Purchase Index however, fell by 10 percent and was 8 percent lower than the prior week on an unadjusted basis. Purchase applications were still their level a year earlier by 11 percent.

Refi Index vs 30yr Fixed

Joel Kan, MBA's Associate Vice President of Economic and Industry Forecasting, provided the following commentary. "The 10-year Treasury yield fell around 20 basis points over the course of last week, driven mainly by growing concerns over a likely slowdown in Chinese economic growth from the spread of the coronavirus.This drove mortgage rates lower, with the 30-year fixed rate decreasing for the fifth time in six weeks to 3.71 percent, its lowest level since October 2016, Refinance activity jumped as a result, with an increase in the number of applications and a spike in the average loan amount, as homeowners with jumbo loans reacted more resoundingly to lower rates."

Loan amounts were up significantly, and the influence of refinancing was clear there as well. The average loan size was $342,400 compared to $319,900 the previous week. Purchase loans rose from an average of $338,700 to $341,400.

Added Kan, "Prospective buyers weren't as responsive to the decline in mortgage rates - likely because of suppressed supply levels. Purchase applications took a step back, but still remained 7.7 percent higher than a year ago."

The FHA share of total applications decreased to 9.6 percent from 10.7 percent the previous week while the VA share fell from 11.7 percent to 10.2 percent. The USDA share dipped to 0.4 percent after weeks at an 0.5 percent share.

Fixed rates, both contract and effective. declined, in some cases decisively, from the prior week. The average contract interest rate for 30-year fixed-rate mortgages (FRM) with loan balances at or below the conforming limit of $510,400 dropped 10 basis points to 3.71 percent. Points were unchanged at 0.28.

The average contract interest rate for 30-year jumbo FRM, loans with balances above the conforming limit, decreased to 3.70 percent from 3.78 percent. Points dipped to 0.19 from 0.20.

The 30-year fixed-rate mortgage backed by FHA had a contract rate of 3.80 percent with 0.26 point. The prior week's average rate was 3.82 percent with 0.27 point.

Fifteen-year FRM had an average rate of 3.19 percent, down from 3.24 percent. Points increased to 0.23 from 0.22.

Adjustable rate mortgage (ARM) products moved higher. The average contract interest rate for 5/1 ARMsincreased to 3.23 percent from 3.15 percent, with points rising to 0.15 from 0.12. The effective rate also increased. The ARM share of total applications still jumped to 5.9 percent. The prior week the share was 4.7 percent.

MBA's Weekly Mortgage Applications Survey been conducted since 1990 and covers over 75 percent of all U.S. retail residential applications Respondents include mortgage bankers, commercial banks, and thrifts. Base period and value for all indexes is March 16, 1990=100 and interest rate information is based on loans with an 80 percent loan-to-value ratio and points that include the origination fee.